SPACs Hit by Broader Market Turbulence

January was the worst month for equities since March 2020 when investors seriously started to anticipate what COVID-19 would ultimately do the economy and market. This poor sentiment in January also spilled over into both SPACs and De-SPAC companies alike.

High growth / low-profitable tech stocks got hammered as the market begins to anticipate rate hikes this year, and De-SPACs joined the ride down. Given that many companies that went public via SPAC fall into the high growth / low profitability bucket, it was not surprising to see such poor performance.

The poor de-SPAC performance has undoubtedly both changed and cooled the M&A market for SPACs. While it was once very easy to raise PIPE financing or drum up investor enthusiasm for a hockey-stick growth co. and take it public via SPAC, that appetite has seemingly fully dissipated. This has led to 1) fewer deals being announced and 2) deal preference shifting to companies with “actual revenue and earnings.”

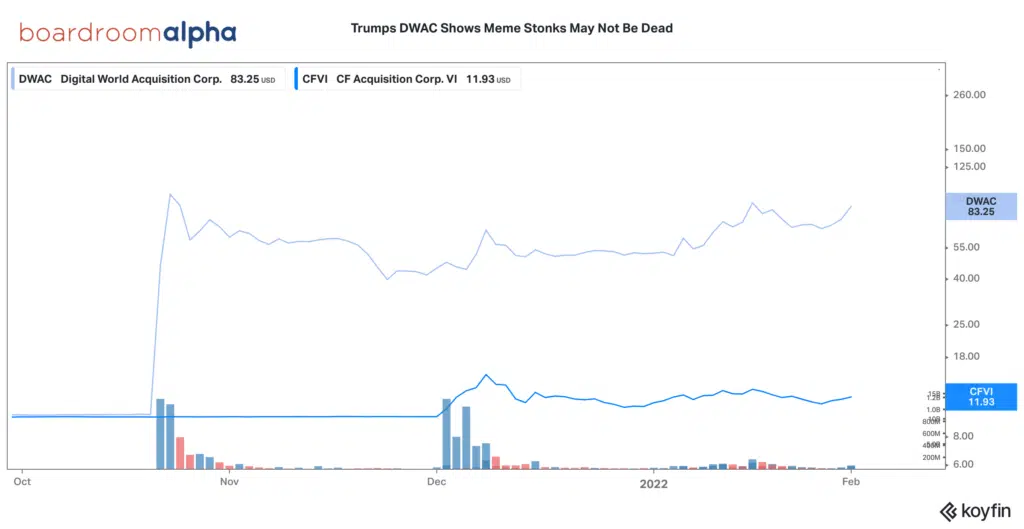

And, for those worried that all SPACs were hit in January, you’ll be pleased to know that DWAC continues to defy the odds and trade like its back in “Peak SPAC” in February of 2021.

Announced SPAC M&A in 2022

There were 12 announced new deals in January totaling over $20.6B in enterprise value.

Some highlights:

- Chamath Palihapitiya returned with 2 new deals from his Social Capital Suvretta SPAC line announcing pacts for both DNAA and DNAC.

- Gary Cohn and Cliff Robbins struck the largest deal of the year thus far with their proposed $9.3B deal for lottery operator Allwyn Entertainment. CRHC also implemented an interesting proposal to entice shareholders not to redeem with gifted shares should they choose to hang on though closing.

- 33% of the deals announced didn’t include a traditional PIPE as part of the financing

IPO Slowdown and Withdrawals

For the last few months we’ve been discussing how the SPAC market is likely overheated with too many SPACs and not enough deals. Yet, despite those dynamics, the SPAC IPO market had roared on with over 50 IPOs in each month since October. However, in January we finally saw that dynamic shift, which is likely to be a positive for the asset class. January priced just 23 SPAC IPOS for a little over $5B. Don’t be surprised to see the market operate on a reduced basis for the next few months as some of the supply continues to get cleared out.

Not only did issuance dramatically slow in January, but also several SPACs that had registration statements on file with the SEC decided to pull their plans for IPO. We saw this dynamic from both repeat sponsors (e.g. Riverside Management pulled 3) and rookie sponsors alike, who want nothing to do with the current pricing dynamics in the SPAC primary market.

Now, to be clear, submitting a registration withdrawal doesn’t mean that these sponsors can’t change their minds and decide to file again, though, it’s pretty telling the number that has creeped up in recent months. Since July we have seen 24 such RW requests, which compares to < 10 for the previous several years.

This aligns with commentary that we’re hearing from investors as many are hitting the pause button on SPACs for the time being, given poor performance across the board.

Money Back Guarantee

Redemptions, redemptions redemptions. That’s been the name of the game thus far in 2022. Who cares the size of your SPAC’s trust account if all 90%+ of the funds will be redeemed? This continuation trend (which we saw happening last year) has undoubtedly led to fewer M&A closures as companies and sponsors are forced to get creative and drum up additional financings to arm companies with the cash they need to grow.

Capstar Special Purpose Acquisition (CPSTR) set the redemption record when they recorded a cool 99% in redemptions on its Gelesis Holdings vote. Overall, SPACs averaged ~80% in redemptions in January 2022, a new record high.

January deSPACs

And, given deSPAC performance, investors won’t be blamed for wanting their money back. January’s deSPACs only have a few bright spots in terms of post deSPAC returns. When measured against return since IPO, only DAVE stands out as a winner so far.

Checking in on Top Sponsors

We’ve long been believers that the solid, repeat sponsors are going to be the ones to have lasting power in SPACs. While we remain steadfast in that belief, even the strong sponsors’ DeSPACs have not been immune to the recent market carnage.

Gores

Gores, with double-digit SPACs to their name, had almost a perfect redemption record coming into their latest vote. Yet even they couldn’t escape the redemption bug when Gores Metropolous II (GMII) got hit with over 90% redemptions on their Sonder deal. After dropping initially on De-SPAC this month, SOND has been clawing back and is trending back towards $10.

Gores is still very active in the SPAC market and don’t be surprised if we see Gores Guggenheim (GGPI) and Polestar inch closer to deal completion. GGPI is one of the few pre-close SPACs that’s been trading at a premium to NAV and that we’d expect to see low redemptions on.

dMY

dMY Technolgy Partners (Niccolo de Masi and Harry You) are long on their way in joining the other SPAC giants. However, their most recent De-SPAC, Planet Labs (PL) has had a bit of a rough go in its first months as a public company, trading < $6 as of this writing.

IONQ has also struggled recently as it came down from its highs last year as “spec tech” broadly fell back to earth. It even briefly traded below SNII, which is IONQ competitor Rigetti Computing public, but has not yet deSPAC’d. However, IONQ has quickly rebounded along with the market and will likely continue to benefit as mood improves and if they are able to hit their targets going forward.

Reinvent Technology Partners

While not historically known as top SPAC sponsors, the Reinvent team is comprised of some of the most well-respected in the VC and tech community including Reid Hoffman and Marc Pincus.

Though as we’ve seen and mentioned, the more VC-esque types of SPACs have been performing terribly as DeSPACs and the reinvent line has suffered with the rest of them.

With all three of their DeSPACs (AUR, JOBY, and HIPO) trading <$5, it’s tough to see them make a push to price their fourth SPAC, RPTX.

State of the SPAC Market

There are still over 580 SPACs out there that are looking for a merger target, and they are still largely trading at a discount to NAV at ~$9.78 for the average common pre-deal SPAC. In fact, rising yields may not be as big a negative for SPACs as some would assume. As rates rise, so too will the rate for SPAC cash trusts that are typically invested in securities that pay that yield. This means that, even despite a rising rate environment, the yield trade for SPACs remain in play, with upside on potential deals.

Which SPAC could be the next to announce a deal? We recently released a Potential Deal Screener that takes into account several factors including a SPAC’s age, time to deadline and OpEx trends to help predict who might be the next deal. Thus far the majority of deals announced in 2022 has scored over 5 on the overall signal.

Who’s Next? Potential Next SPACs to Announce

SPAC Calendar for February

January ended with ECP Environmental Growth Opportunities Corp (ENNV) slashing their deal valuation for Fast Radius by 25% from $1B to $750, and adjourning their shareholder vote meeting until 2/3. That helps to kick off what will set up to likely be a busy month for merger votes / DeSPACs with 13 on tap thus far.

Know Who Drives Return Podcast

Boardroom Alpha’s team talks to the public company and SPAC leaders that are driving return for shareholders, delivering on ESG promises, and more.

See all the episodes here and make sure to subscribe using your favorite podcast app so you don’t miss a single episode.

Recent podcasts

- Update on Activism and Universal Proxy with Michael R. Levin

- AON’s Aria Glasgow on Managing ESG and Human Capital Risk

- Korn Ferry’s Anthony Goodman on the Importance of Board Evaluations

- Podcast: Getaround CEO Sam Zaid on Carsharing and Going Public

- What to Know about Universal Proxy with Bruce Goldfarb of Okapi Partners

- Podcast: Li-Cycle’s (LICY) Ajay Kochhar on Lithium Ion Battery Recycling and EVs

The Daily SPAC

Boardroom Alpha publishes daily SPAC market analysis at theStreet.com. Sign up for the newsletter and get it in your inbox daily.

SPAC Monthly Market Reviews

- SPAC Market Review – April 2023

- SPAC Market Review – March 2023

- SPAC Market Review – February 2023

- SPAC Market Review – January 2023

- SPAC Market Review – December 2022

- SPAC Market Review – November 2022

Contact Boardroom Alpha

Contact the Boardroom Alpha team to learn more about the SPAC Intelligence Service or learn more about the monthly SPAC report.

Sales: sales@boardroomalpha.com

Customer Success: customersuccess@boardroomalpha.com

Disclaimer

The opinions and information contained herein have been obtained or derived from sources believed to be reliable, but Boardroom Alpha cannot guarantee its accuracy and completeness, and that of the opinions based thereon.

This report contains opinions and is provided for informational purposes only – it does not constitute investment, legal or tax advice. You should not rely solely upon the research herein for purposes of transacting securities or other investments, and you are encouraged to conduct your own research and due diligence, and to seek the advice of a qualified securities professional before you make any investment.

None of the information contained in this report constitutes, or is intended to constitute a recommendation by Boardroom Alpha of any particular security or trading strategy or a determination by BA that any security or trading strategy is suitable for any specific person. To the extent any of the information contained herein may be deemed to be investment advice, such information is impersonal and not tailored to the investment needs of any specific person.

No representation or warranty, expressed or implied, is made on behalf of Boardroom Alpha as to the accuracy or completeness of the information contained herein. Boardroom Alpha does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed.