“SPAC mergers are getting announced, but there isn’t much for the market to get excited about,” said Boardroom Alpha’s David Drapkin. While it’s encouraging to see a large deal announced, “Bestpath is just another example — a tiny trust, no committed financing, and quite speculative in the EV space,”

https://www.bloomberg.com/news/articles/2023-03-29/chinese-vehicle-spac-deal-marks-return-of-billion-dollar-mergers

Our quote above from a recent Bloomberg article about sums it up for SPACs. The SPAC market continues to inch along at a slower and smaller pace, but there is little excitement at the moment for any participant.

On a (slightly) positive note the market is inching towards right sizing itself. Following another round of liquidations, Pre-Deal SPACs are <300 for the first time in recent memory. In addition, the great maturity wall of March ’23 has now passed and SPACs can get back to focusing on finding merger targets, rather than soliciting proxies for the deluge of extension meetings that have taken place over the last 4-6 months. Though, we’ll see extensions continue and will hit another series of votes unless the pace picks up.

We recap March’s SPAC market activity below.

SPAC Mergers

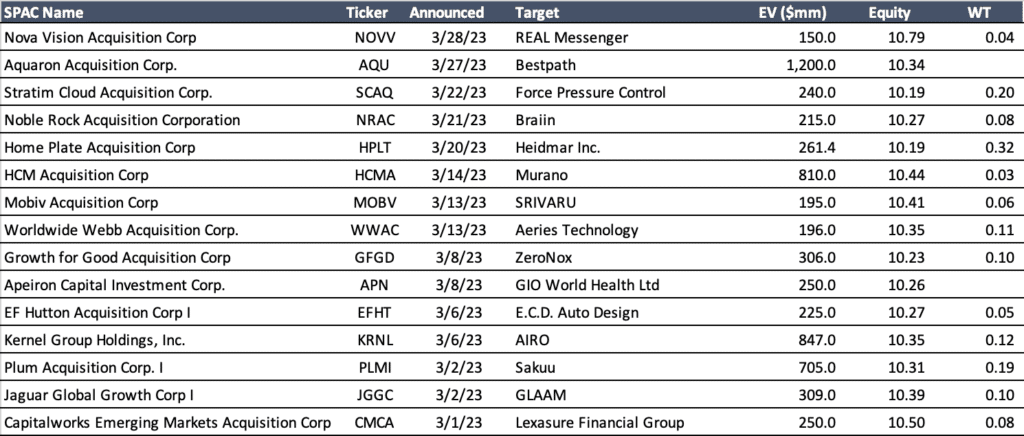

Announced SPAC merger activity remained on pace with recent months with 15 new deals announced. As has been the case for most of the last year, none of the month’s new deals were announced with an already agreed upon traditional PIPE financing.

In the deal announcements, several SPACs stated that they are searching for additional financing to be added at a later date. Given the state of markets and macro, that financing could be hard to come by. More broadly, until committed financing at SPAC deal time returns, it will be tough to garner support from public shareholders. As you can see in the latest equity prices below, there has been little enthusiasm from public market shareholders to the M&A.

The largest deal of the month came with Aquaron Acquisition Corp. (AQU) striking an agreement with Bestpath a Chinese hydrogen fuel cell powered vehicle company. It was the first > $1B sized deal since Pono Capital Two (PTWO) and SBC Medical Group in early February. Our quote above about sums up our, and the market’s, take on the deal though.

SPAC IPOs

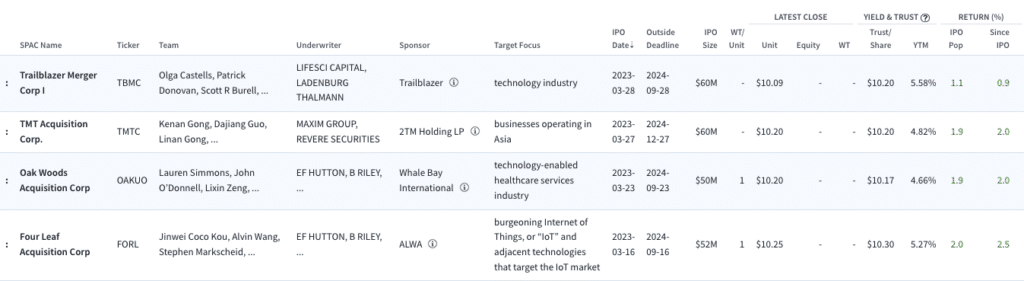

March 2023 SPAC IPOs

The SPAC IPO market continues to putter along with just a handful of new SPAC IPOs coming each month, all at much smaller sizes than during boom times. Four new SPAC issues hit the market in March all less than $75M. In addition the bulge bracket banks are still on the sideline for the time being.

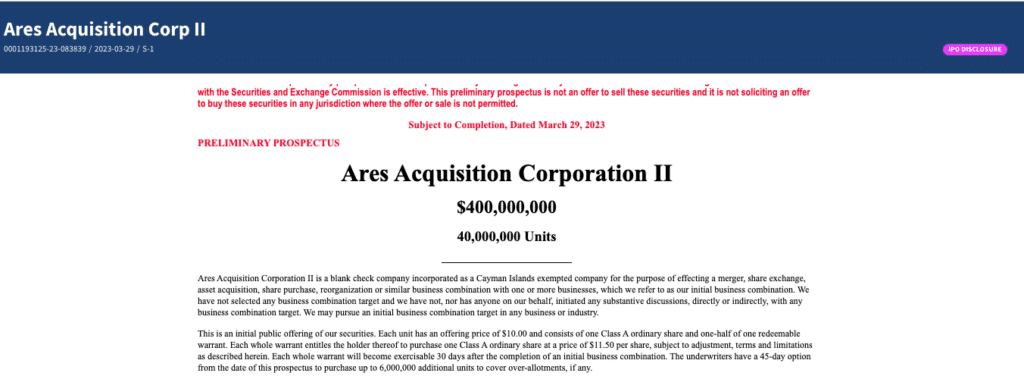

That being said, Ares recently filed an S-1 for a new SPAC, Ares Acquisition Corporation II. The prospectus calls for a $400M raise with Citigroup and UBS on the books. It would be a welcome sight to see a new issue from a reputable sponsor and bulge bracket banks.

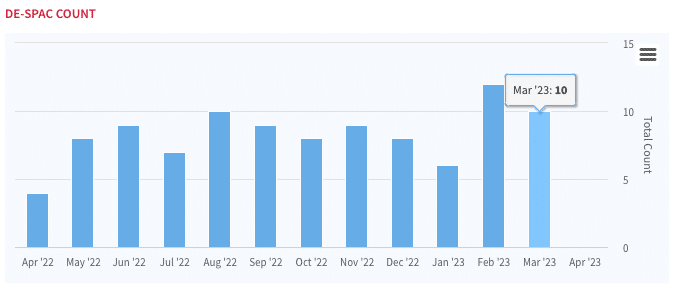

DeSPAC’ing

10 deals made it across the finish line in March, slightly below February’s level. Redemption rates remain elevated as 95% of trust capital was redeemed for all of March’s deals, which was a slightly up from earlier in 2023. As we’ve said many times before, with redemptions that high it shows there is no interest from the broader market to invest in the deals beyond deSPAC and it hamstrings the combined company given the SPAC’s trust is drained and so provides little cash to the post-deSPAC to accelerate the business. Those that have DeSPAC’ed are largely down since ticker change — a trend we don’t see changing for some time yet.

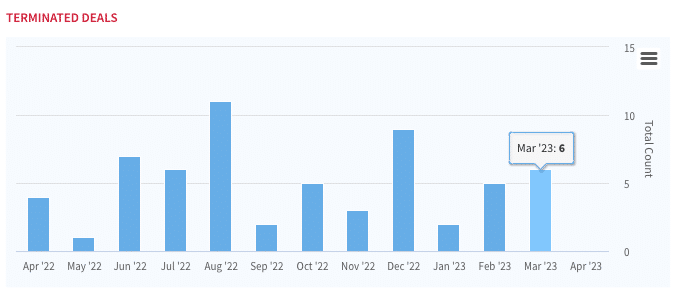

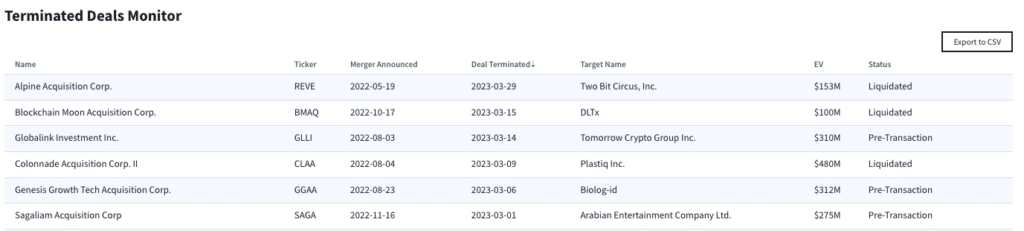

It remains difficult to get SPAC deals over the line and deal terminations ticked up in March with 6. SPACs such as Alpine Acquisition Corp. (Two Bit Circus) and Blockchain Moon Acquisition (DLTx) ultimately chose to close up shop and liquidate rather than continuing chasing debilitating extensions.

What’s Next?

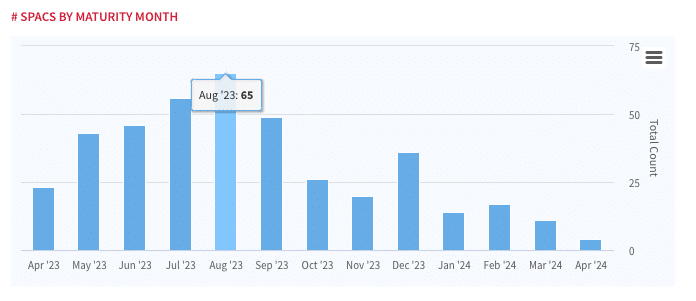

Look out for the next maturity wall in August of this year. It is very likely that a vast higher majority of SPACs will decide to liquidate rather than extend if they are unable to find a merger target over the next several months. This will be especially true if there remains significant uncertainty around risk on / risk off markets, FED rates, and the overall macro picture.

And in the near term SPAC extension votes and liquidations keep coming…