Lucid (LCID) stock is running hot into its Q4 earnings report, today aftermarket. The big question is what investors are willing to pay for growth.

Key points ahead of the quarter

First cars on the line. Impressive reservation numbers. Consensus calls for $(0.30) on $59.87 million. In Q3, LCID exceeded 13,000 vehicle reservations, for an estimated order book of over $1.3 billion. Customer vehicle production of Lucid’s first car, the Lucid Air, also began in Q3 and deliveries began on October 30.Demand appears to be accelerating as the company ramps up production capabilities at its AMP manufacturing facility in Casa Grande, Arizona. Customer reservations increased to 17,000 as of November 15.

High operating expenses will impact earnings and cash flow. Will it matter? Given where Lucid is in its production lifecycle, we would expect high technology and product development expenses to have negatively impacted margins this quarter. The company has already announced spending to expand capacity of its Arizona manufacturing facility as well as new retail and service locations. In Q3, R&D and SG&A costs increased over 80% and 800% respectively from year-ago levels. Investors may believe in the cars and the growth trajectory, but the bottom line is that Lucid is generating high CAPEX and OPEX expenses without meaningful revenues right now.

Signs $30 million lease agreement on Saudi plant. Today, the company announced a $30 million lease agreement with Emaar Economic City for an industrial plot in King Abdullah Economic City outside Jeddah. Chairman Andrew Liveris had previously revealed plans to have an EV factory in Saudi Arabia by 2025 or 2026.

No doubt, Lucid can sell every car that comes off the line right now… Last quarter, LCID reiterated its expectation of delivering 20,000 cars in 2022. Given that reservations were 17,000 in November, it’s not unreasonable that the company could easily have added another 2,000 new pre-orders a month. We expect that when the company updates its pre-order number, it should handily exceed the company’s 20,000 manufacturing capacity figure.

…but production is the key risk here. LCID recently reported a recall of 203 Airs owing to a safety issue concerning the front strut damper, which was assembled improperly. Note that while Lucid has begun to deliver the Air, it has yet to announce deliveries of its second most expensive car, the Grand Touring.

European expansion update. Lucid will expand throughout Europe this year. The company has been taking online reservations from customers in Austria, Belgium, Denmark, Finland, France, Germany, Iceland, Italy, Monaco, Netherlands, Norway, Spain, Sweden, Switzerland and the United Kingdom. Specific delivery information by country is expected shortly.

Balance sheet update. LCID significantly strengthened its balance sheet, closing the de-SPAC merger and PIPE– bringing in approximately $4.4 billion to the balance sheet. The company ended last quarter with $4.8 billion in cash.

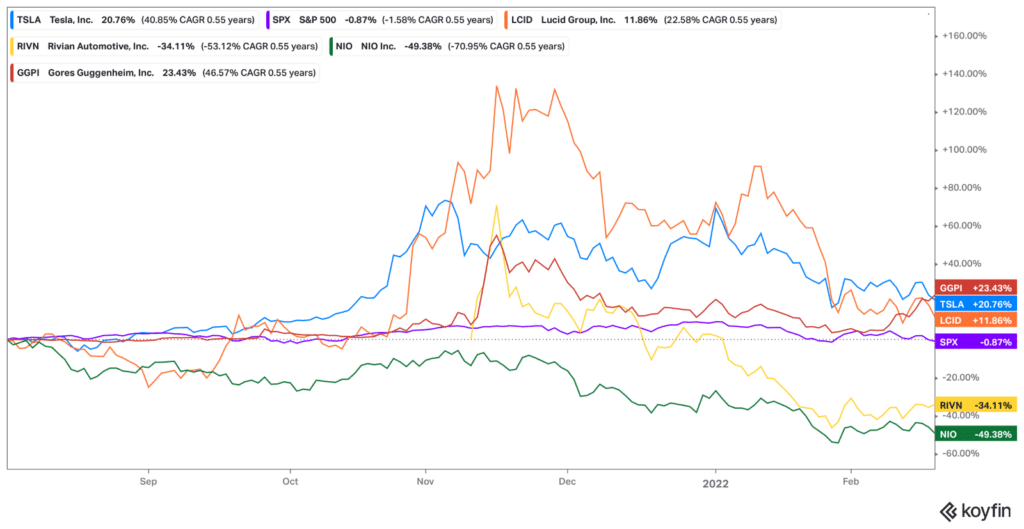

LCID stock has plunged 40% YTD, but still see downside risk at these levels

Broader sector selloff not helping. Despite reiterating 20,000 unit guidance, LCID shares have plunged ~40% since the start of the year—in part owing to a broader sector sell-off, which has impacted names including Tesla (TSLA), Rivian Automotive (RIVN), and Nikola (NKLA). Then of course there’s the unpleasant macro of rising commodity prices, a dampening global economic outlook, and a more cautious U.S. Federal Reserve worldview when it comes to tightening monetary policy.

EV Performance: Not surprisingly, LCID, RIVN have been the most volatile of the group

Challenging times for carmakers, even bellwether TSLA. Even sector bellwether Tesla isn’t immune to the macro. Despite reporting record earnings ($5.52 B in net income), quarterly operating margin of 14.7% and delivering an 87% YoY increase in deliveries, Tesla stock has declined 27% YTD. Note that RIVN missed its own modest 2021 production guidance of 1,200 vehicles (the company manufactured 1,015 vehicles).

Cost concerns as LCID moves to ship multiple models at low volume. Tesla’s earnings commentary surrounding supply chain challenges and an ongoing chip shortage underscores the possibility that smaller carmakers could have difficulties ramping their production this year. Lucid may face challenges and higher than expected costs as the company attempts to produce lower volumes of four different versions of the Air. In contrast, Tesla has the advantages of strong demand; 2) virtually non-existent advertising costs; and 3) production efficiency. Shipping and logistics costs are also a concern as Lucid still lacks a sophisticated distribution system as it ships vehicles across the country.

LCID is still a high-risk, retail-driven momentum story. We prefer GGPI. Despite “best in class” blend of range, performance, and charging technology, we don’t see LCID as particularly well insulated from the multiple negative headwinds we’ve outlined. We continue to view LCID as a high-risk stock. While it can be argued that TSLA stock is priced for perfection and that no one expects LCID to ship 1 million cars anytime soon, still– LCID’s $47 billion valuation looks extremely rich for a company that is still years away from generating positive operating income. The company is only just beginning to ramp sales and scale production. High OPEX and CAPEX and limited visibility into profitability are key concerns. We also view LCID’s luxury positioning as a niche market—particularly relative to new companies such as Polestar (GGPI), which plays at broader price points (low-to-high). We’re more inclined to buy GGPI here ahead of its upcoming SPAC merger. We view risk/reward as unfavorable on LCID and think the stock could re-test the $20 levels.

Hear Polestar CEO Thomas Ingenlath on the Know Who Drives Return Podcast

Read our full report on Polestar (GGPI) here.