Ryan Cohen hopes for a GameStop re-run at this short-squeeze favorite. Right now, it looks more like a meme stock and less of a turnaround.

Ryan Cohen, billionaire co-founder of online pet-product retailer Chewy Inc. (CHWY) has taken a 9.8% stake in Bed Bath & Beyond (BBBY) through his investment firm, RC Ventures LLC. Cohen is pushing for the housewares retailer to streamline its strategy and explore strategic alternatives, including full or partial sale.

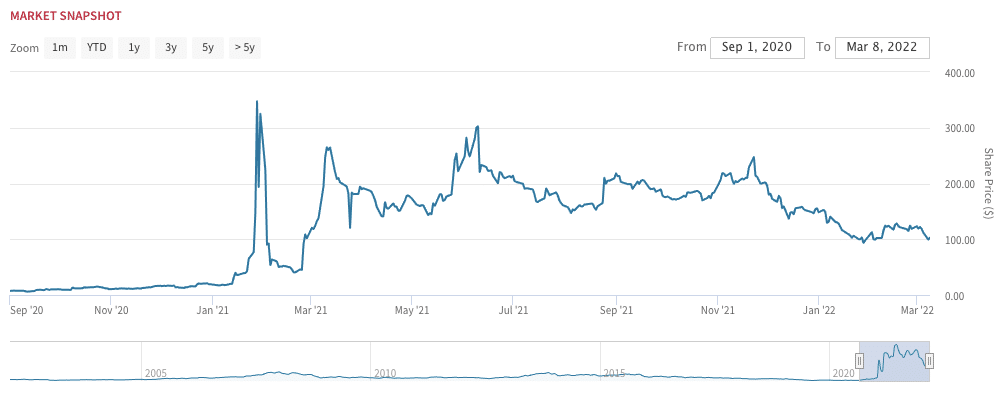

GameStop vibes. Cohen serves as chairman of videogame retailer GameStop Corp. (GME). While not your typical activist, “Papa Cohen” has built a loyal retail investing following on social media for his unconventional style. Cohen’s BBBY stake is reminiscent of similar moves at GameStop in late 2020. At the time, Cohen disclosed a nearly 10% stake in the videogame retailer through his investment firm RC Ventures LLC. He sent a letter to the GameStop’s board, urging the company to improve its e-commerce and explore other tech-driven strategies. In January 2021, Cohen was added to GameStop’s board. In April, he became chairman. His addition to the board caused a gamma squeeze in GameStop shares, sending them to an intraday high of $483 last year from below $20 a share at the start of the year. In recent quarters, however, Cohen has been fairly quiet about his turnaround strategy at the game retailer.

Betting on what, exactly? In addition to stock ownership, it’s important to point out that RC Ventures also bought out-of-the-money BBBY call options with expiration dates of January 20, 2023 that require ~ 5x gain in the share price to pay off. Hard not to ask yourself if a meme stock squeeze wasn’t part of the thinking here.

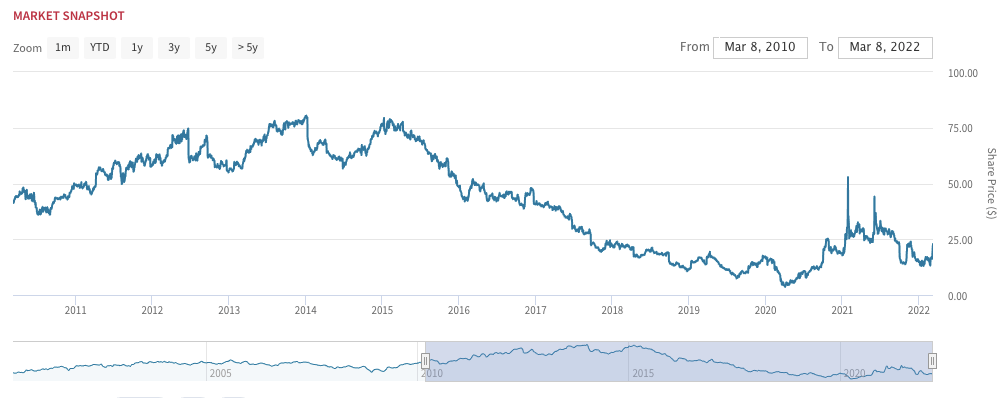

BBBY stock: Last year’s meme stock favorite is down 70% from all-time highs. Throughout 2021, BBBY was similarly buoyed by the meme stock craze. However, the company’s inconsistent performance– exacerbated by slowing sales and earnings miss and guidance cut in Q3 — doomed several retail-driven momentum rallies. BBBY stock currently trades ~$23 per share, down over 70% from an all-time high of ~$80 reached in 2013.

Revenue growth down YoY, suggesting market share loss. BBBY operates hundreds of stores throughout the country as well as the Buybuy Baby and Harmon retail chains.BBBY’s turnaround plan includes reducing the number of products in its stores as well as launching new private-label brands. Like many retailers, BBBY suffered from supply-chain issues which resulted in lost market share to Amazon (AMZN) and Target (T). The company also made other missteps, such as cutting back its promotional mailers too drastically, which in turn hurt sales.

As Cohen points out, BBBY has suffered from sustained market share losses, pointing to a 14% decline in YoY sales in the company’s most recent quarter. BBBY reported sales of $16.4 billion– the low end of the company’s guided range issued back in late November. Several headwinds have impacted the consumer electronics retail sector, including the rise of the omicron variant, and inflation.

Slowing growth and rising expenses: not a good combination. Guidance calls for sales to decline to $49.3 billion – $50.8 billion, down from $51.8 billion for 2021. Management commented on the potential for reduced demand continuing into 2023. While top line growth is slowing, selling expenses have increased, owing to increased advertising and new spending on the company’s digital sales platform. The combination of reduced growth and increased spending suggests reduced earnings growth for the foreseeable future.

Cohen pushing for more focused turnaround and sale. Cohen wants to see the company do 4 things: 1) narrow the focus of its turnaround plan; 2) maintain the right inventory mix to meet demand; 3) explore a separation of the Buybuy Baby chain or a sale of the entire company; and 4) align executive compensation more closely with corporate performance. He argues that Buybuy Baby could be worth several billion dollars. Cohen also thinks the entire company would be better off in the hands of a private-equity firm. In a statement Monday, BBBY acknowledged Cohen’s letter, stating “while we have had no prior contact with RC Ventures, we will carefully review their letter and hope to engage constructively around the ideas they have put forth.” Cohen, based on yesterday’s Twitter feed, isn’t pleased by the lack of direct communication:

We think an outright sale would be tough unless earnings improve significantly. BBBY maintains a relatively healthy operating margin: 6% for 2021, which is flat on a YoY basis. However, there is mounting pressure on Best Buy’s profitability right now. Gross margins declined by almost a full percentage point in Q4 as the company eased some of its services pricing. Selling expenses have also increased, owing to increased advertising and new spending on the company’s digital sales platform. Operating income declined to $803 million, or 4.9% of sales, compared with $1 billion, or 6.1% of sales, in late 2021.

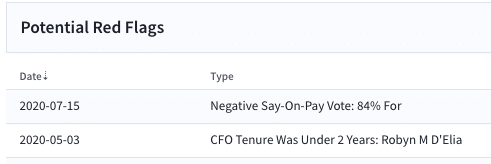

Red flags: Executive compensation and Board experience. Cohen has a point when it comes to executive compensation. Say-on-pay vote was 84% in favor (7/2020). In July 2020, the company adopted a short-term incentive plan consisting of cash-based pay-for-performance incentive compensation to employees and company officers. Cohen points out that BBBY’s executive officers were collectively awarded nearly $36 million in compensation last fiscal year — “a seemingly outsized sum for a retailer with a nearly $1.6 billion market capitalization.” Former CFO Robyn D’Elia was fired less than two years into the job in 2020 as COVID was forcing store closures. Cohen states that given his involvement with GameStop prohibits him from becoming a BBBY director himself; but he doesn’t rule out his firm nominating directors. Notably, the nomination window is open now and closes mid-March.

BBBY red flags: Cohen could push for new directors

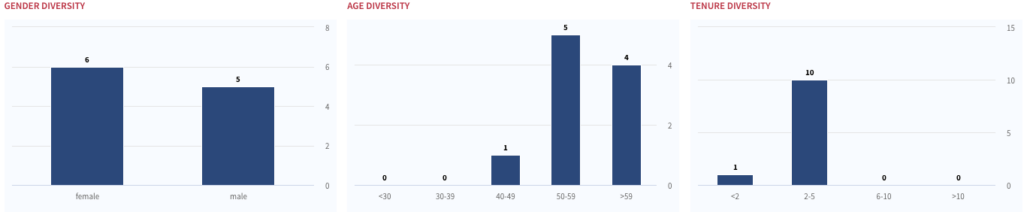

The company’s board is relatively new having been refreshed in 2019 as part of a shareholder push to revamp an entrenched board. The only director to have been serving more than 3 years is Virginia Ruesterholz, who has been serving since 2017.

BBBY: Board Diversity and Inclusion Snapshot

As fundamentals-based investors, there’s nothing to see here right now.

We aren’t buying the squeeze, and we’re not calling this a turnaround story. Short interest at BBBY is still high at ~26% of float. While that’s down from the more than 60% short interest reported before last year’s meme-stock frenzy, it’s still up from levels we saw late last year. Cohen’s investment and bravado may certainly scare short sellers for now, pushing the stock upward. But at the end of the day, fundamentals matter. Without evidence of improving revenue growth and profitability, we don’t see any compelling reason to get interested. With BBBY’s top and bottom-line growth likely to struggle over the next 12 months, we aren’t willing to jump into the stock as a turnaround story. “Papa Cohen” effect aside, we’d argue the stock is dead money for now.

BBBY: Insider buying up considerably over the last 12 months. Insider buys totaled $2.6 million over the past 12 months. Clearly more buying than selling, with several executives and Directors making purchases in January of this year when the stock was in the low teens. Insiders own ~2.7% of the company, suggesting relative alignment between insiders and shareholders.

BBBY: Insider trading activity

Most of BBBY’s mistakes look like they’re behind the company. To be clear, BBBY would probably have weathered 2021 better had it prioritized supply chain and IT modernization over other strategic priorities. But management has essentially come clean with its mistakes, and most of the supply chain stresses are now behind the company. While changes in executive compensation may be warranted, they won’t change the trajectory of the business.

GameStop: Crickets from Cohen. Cohen’s last public comments on GameStop—aside from a few cryptic tweets and memes—were at a shareholder meeting in June of last year, when he outlined goals for driving shareholder value for the long term. “You won’t find us talking a big game, making a bunch of lofty promises or telegraphing our strategy to the competition,” Cohen said. “That’s the philosophy we adopted at Chewy. He concluded his remarks with “Buckle up.” Almost nine months later, GameStop shares are down ~ 50%. While BBBY shares are up ~44% since the news of Cohen’s involvement with the company, GME is down ~6% over the same period.

GME is Down Big Since its Highs