While COVID-related issues are abating, it’s no secret that many companies are still struggling to find their footing. We take a close-up look at 5 long-tenured CEOs (+ 1 co-CEO) that are facing big negative 3-year returns.

We examine 5 public companies delivering negative 3-year TSR with with CEO tenures of greater than five years. Interestingly, the top two underperformers — Netflix (NFLX) and Warner Brothers Discovery (WBD)– are both in the streaming entertainment business; VF Corp. (VFC) is an apparel manufacturing story with potential brand weakness; Illumina (ILMN) is a life sciences diagnostics player facing competition and potential acquisition risk; and Okta (OKTA) is a cloud-based security software story with a murky path to profitability.

Can the Long-Tenured CEOs at NFLX, WBD, V F Corp, Illumina, and Okta Turn Things Around?

Key Points:

While the end markets and business models of these companies differ significantly, each is facing significant competitive shifts impacting financial performance which include:

- product and technology shifts

- adapting to an evolving competitive landscape

- new product introductions

- operating expense control

- acquisition / integration risk

- M&A / regulatory risk

Companies on this list have CEO tenures of at least 5 years. Interestingly, all but one of the companies in this list (the exception being OKTA) have concerns around executive compensation. EBITDA and FCF growth for the group is trending negative as the group works to manage large, dilutive acquisitions and faces product transitions. Increased competition plays a role at each of these companies, which means that management will have to balance operating expenses with future growth. Here’s a closer look.

Netflix (NFLX): Reed Hastings and Co-CEO Ted Sarandos

- Sector: Entertainment

- CEOs: Reed Hastings (23.8 years) and Ted Sarandos (1.9 years)

- CFO: Spencer Neumann (3.4 years)

Weaker macro pressuring streaming giant. Streaming entertainment service company Netflix is headed by co-CEOs Reed Hastings and Ted Sarandos. Hastings cofounded Netflix along with Marc Randolph in 1997. Sarandos has been at the helm for just under 2 years. Netflix provides subscription service streaming movies and television episodes over the Internet as well as a DVD by mail service. The company operates 3 business segments: domestic streaming, international streaming and domestic DVD.

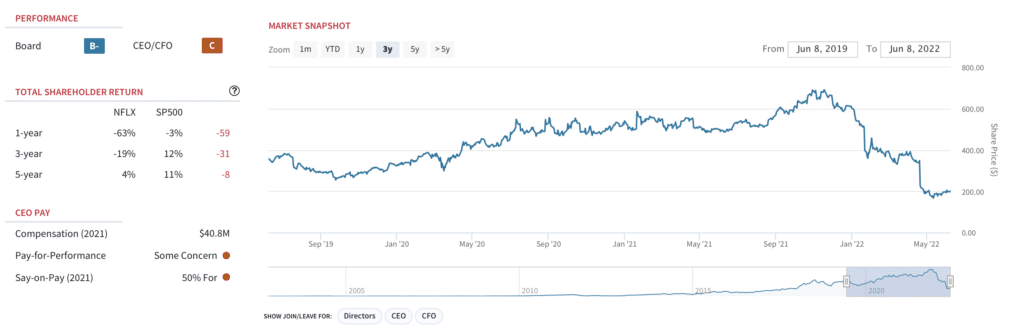

NFLX shares under pressure since reporting Q1 subscriber loss and weak Q2 guidance. NFLX shares have declined 63% over the past year, versus a 3% decline for the S&P 500 over the same period. In the most recently-reported Q1, Netflix lost 200,000 paying subscribers and expects to lose another 2 million in Q2. Recent initiatives to protect revenues — such as price increases and preventing password sharing– haven’t been well-received in a recessionary environment.

NFLX: Market snapshot

Increasing streaming competition. Content is extremely fragmented and Netflix faces increasing competition from Amazon (AMZN), which has moved more aggressively into video streaming. Other emerging players include HBO Go and Vudu, which is partnered with Walmart (WMT).

NFLX Co-CEO Ted Sarandos: Performance scorecard

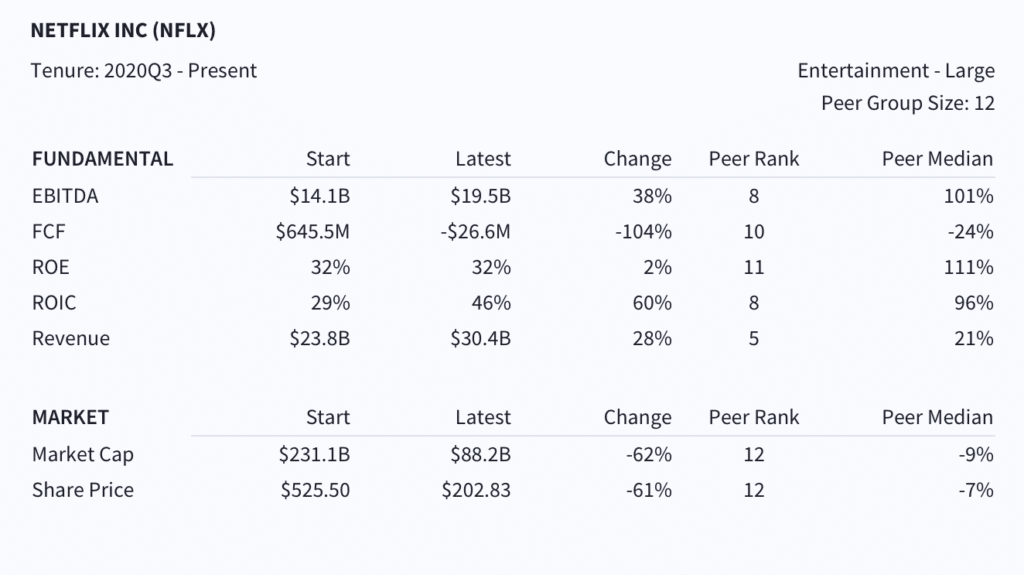

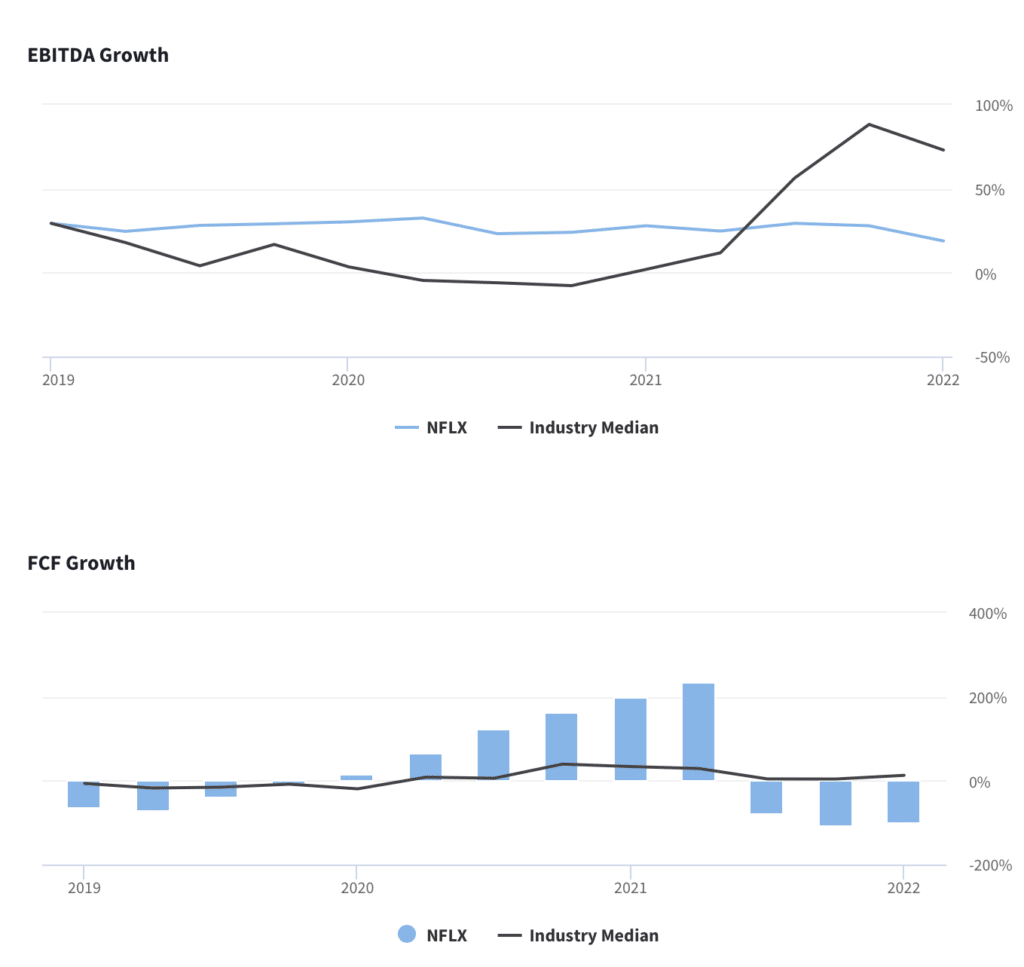

EBITDA and FCF trending below peers. Netflix’s EBITDA growth has been declining since Q3 2021. EBITDA growth was +19% YoY in the most recently reported Q1, versus industry median of +73% and +28% in the year-ago quarter. FCF growth has been negative since Q3 2021. For Q1 2022, FCF declined 101% YoY, versus an industry median of +13% YoY.

NFLX: EBITDA and FCF Growth

Red flag: Executive compensation. Some concern here, as 2021 CEO compensation was $40.8M– well above the peer median. Last year’s compensation for Netflix CFO Spencer Neumann was $12.5M– in line with TSR and financial metrics, but high relative to peers. Directors are paid in-line.

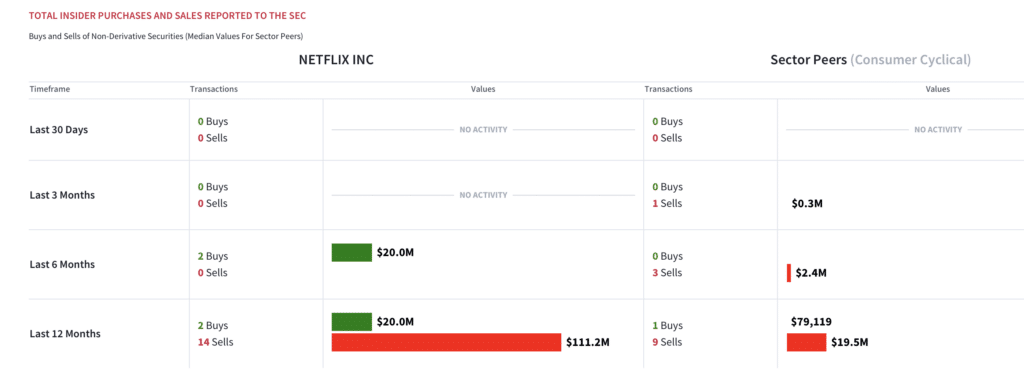

NFLX: Insider trading snapshot

Roku takeout speculation. Speculation continues surround a potential acquisition of streaming player Roku (ROKU), whose shares have declined 68% year-to-date. For Netflix, a Roku acquisition would give the company a presence in advertising-supported streaming. That said, there are very few synergies between the two business. Importantly, Roku is unprofitable (and also makes physical devices), which would imply a dilutive acquisition.

Warner Brothers Discovery (WBD): David Zaslav

- Sector: Entertainment

- CEO: David Zaslav (15.4 years)

- CFO: Gunnar Wiedenfels (5.2 years)

Newly formed streaming entertainment giant. Warner Brothers Discovery (WBD) is number two on the list, but it’s important to point out that in many ways, this is a new company. WBD was formed by the April spin-off of AT&T’s media business, WarnerMedia– which was then merged with Discovery. CEO David Zaslav spearheaded the transaction, having previously served as CEO of Discovery from 2006 until the merger. Now, Zaslav is navigating the next stage in the new media giant’s future. For WBD, the integration of assets should generate significant cost and sales synergies while creating a best-in-class content library. HBO Max and Discovery+ had 74 million and 22 million streaming subscribers at the end of 2021, respectively. HBO Max is the third largest platform by market share. WarnerMedia’s combination of live sports, news, premium television, and scripted shows is already strong– and Discovery brings a highly differentiated set of channels from HGTV to Discovery to Food Network that not only attract complimentary demographics, but also are effective at driving advertising. The merger also brings cable TV channels and the Warner Brothers Hollywood studio.

Shares have declined sharply since the spin-off from AT&T. Despite the synergies, the newly created entertainment giant has faced executive upheaval in the midst of trying to achieve its financial targets. A slew of WarnerMedia corporate executives have left the company since the deal was announced. WBD shares gave declined 16% over the past three years– versus +12% for the S&P 500 over the same period (of course, this includes performance prior to the spin-off/merger). Since the $43B transaction closed in April, WBD shares have declined 43% (versus -18% for the S&P500). Zaslav’s primary directive: finding $3 billion in cost-saving synergies while expanding the number of movies the company produces. Zaslav plans to take on Netflix (NFLX) and Walt Disney (DIS) in the streaming space. Notably, Zaslav has a good merger integration track record, having been responsible for extracting upside to synergy targets associated with Discovery’s 2018 acquisition of Scripps Networks Interactive.

WBD: Market Snapshot

Red flag: executive compensation. Zaslav was paid $246.6M in 2021– well above TSR, financial metrics and the peer median. Similarly, CFO Wiedenfels took home 2021 compensation of $11.3M — well above comparables. Directors were paid $0.3M on average, well above TSR but in-line with peers.

Well-positioned longer term. AT&T has previously forecast 2022 revenue for WarnerMedia of $36.7B; Discovery has guided to $13.1B. On a combined basis, that equates to $49.8B, below DIS, which reported $67.4B in revenue last year, and Paramount Global, at $28.6B. The upward end of consensus estimates forecasts 200 million global subscribers for WBD over the next few years– versus 222 million Netflix subscribers at the end of 2021. In addition, a high-quality content library and strategic partnerships offer long-term strategic advantages.

VF Corp. (VFC): Steven Rendle

- Sector: Apparel Manufacturing

- CEO: Steven E. Rendle (5.4 years)

- CFO: Matthew Puckett (1.0 years)

Diversified portfolio of active lifestyle brands. VFC owns a diversified portfolio of activity-based and apparel and footwear brands, including Vans, The North Face, Timberland, Jansport and Smartwool. The company has a market capitalization of $18B and generated 2021 sales of $11.8B for F2022 (Apr).

Shares under heavy recent pressure; recently revised guidance. Shares have declined 16% over the past 3 years, versus a 12% gain for the S&P 500 over the same period. Last month, the company issued revised F2023 earnings guidance of $3.30-$3.40 on revenue of $12.67B. Revenue is expected to be up at least 7% in constant dollars in the fiscal year ending March, which was lower than consensus estimates of ~10% YoY growth.

Strong dividend payer with >4% yield. VFC currently pays a 4.23% dividend, with a 2022 payout of >60%. The company has a 48-year history of consecutive dividend raises.

VFC: Market snapshot

High freight costs, China COVID lockdowns, and underperforming Vans brand. Investor concerns center around trends in the Vans footwear business and an $845 million payment to the IRS related to a tax dispute that VF anticipates for this year. VFC’s active segment, which is driven by revenue from its Vans brand, missed consensus revenue expectations — generating ~$1 billion in revenue in the most recently reported Q1 (+ 2% YoY) versus guidance of over 5%. In contrast, other brands are performing well. The North Face brand grew 26% YoY, well above 16% guidance. The company is focused on refreshing the Vans brand and expects China restrictions to ease beginning in June. But it remains unclear if this is a temporary hiccup or potentially a bigger issue affecting the Vans brand.

The good news is that margins are still holding up. Despite a recent quarterly earnings miss and reduced outlook, gross margin for F2023 is expected to be up by about half a percentage point– in line with prior guidance of an increase of 0.4 to 0.5 percentage points.

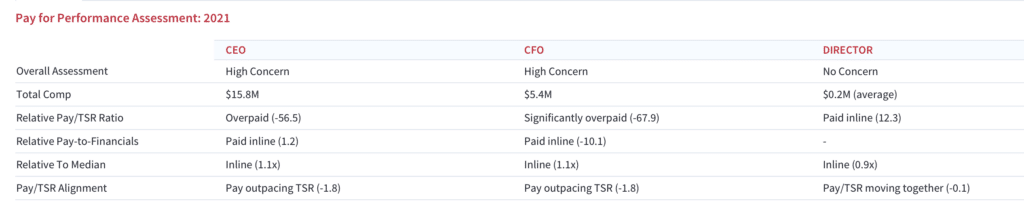

Red flag: Executive compensation. CEO and CFO compensation are well above peer median relative to TSR and financial performance. Rendle was paid $15.8M in 2021; CFO Matthew Puckett was paid $5.4M in 2021. Director compensation is in-line.

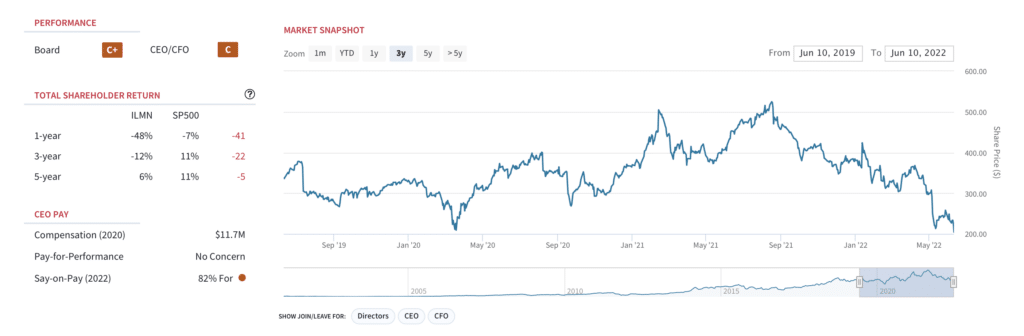

Illumina (ILMN): Francis Desouza

- Sector: Diagnostics & Research

- CEO: Francis Desouza (5.9 years)

- CFO: (outgoing, 5.5 years)

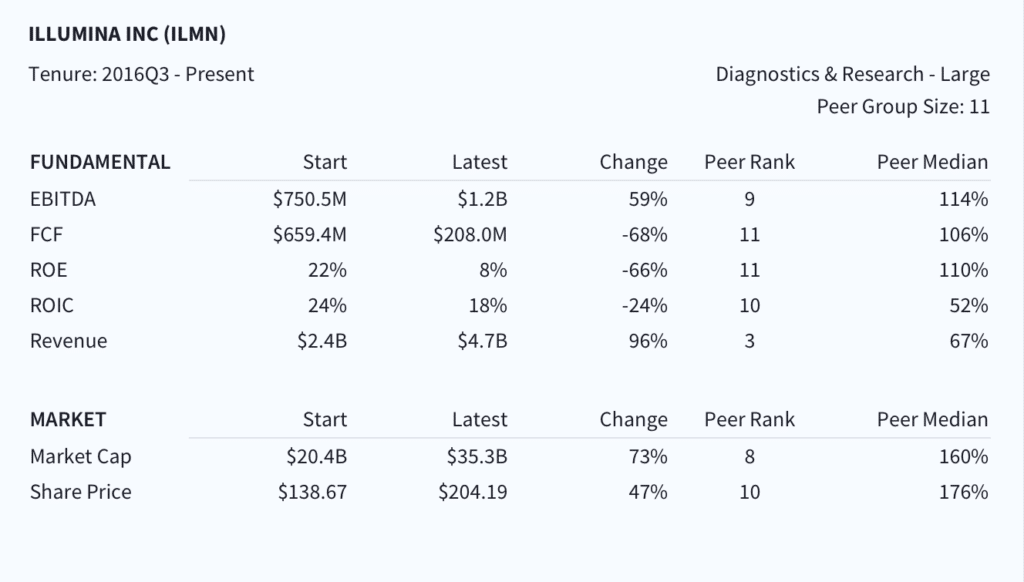

Expanding beyond genetic sequencing. With a market capitalization of $31B, Illumina makes diagnostic equipment that can “read” DNA to help identify genetic factors tied to cancer and other diseases. The company is looking for growth and expansion beyond its core DNA sequencing business into blood-based cancer screening and new drug discovery. Key to this strategy is Illumina’s $7.1 billion acquisition of Grail, a maker of a non-invasive, early detection liquid biopsy test that can screen for multiple types of cancer in asymptomatic patients at very early stages using DNA sequencing. Global demand for genetically-informed cancer treatment has increased in recent years as clinicians work to better understand disease development and progression.

ILMN: Market Snapshot

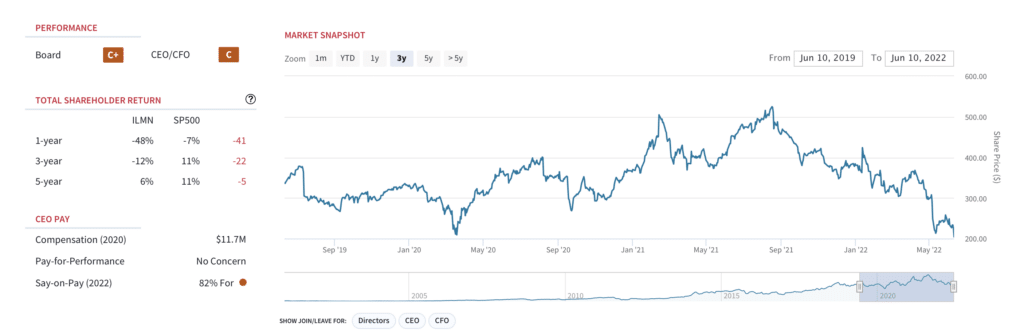

ILMN shares have underperformed over the past 1, 3 and 5-year period. ILMN shares gave declined 48% year-to-date, versus a 7% decline for the S&P 500 over the same period. Shares have similarly underperformed over a 3-year and 5-year period. In ILMN’s most recently reported Q1(Mar), sales and earnings beat consensus forecasts, but revenues were in-line. For the full year, Illumina is guiding to revenue growth of 14%-16% YoY. Growth has been negatively impacted by China lockdowns, which reduced March quarter sales by ~$10M and are expected to trim ~3 percentage points from Q2 top line growth. Q2 guidance calls for revenue growth of 10%-to-12% YoY.

ILMN CEO Francis Desouza: Performance Scorecard

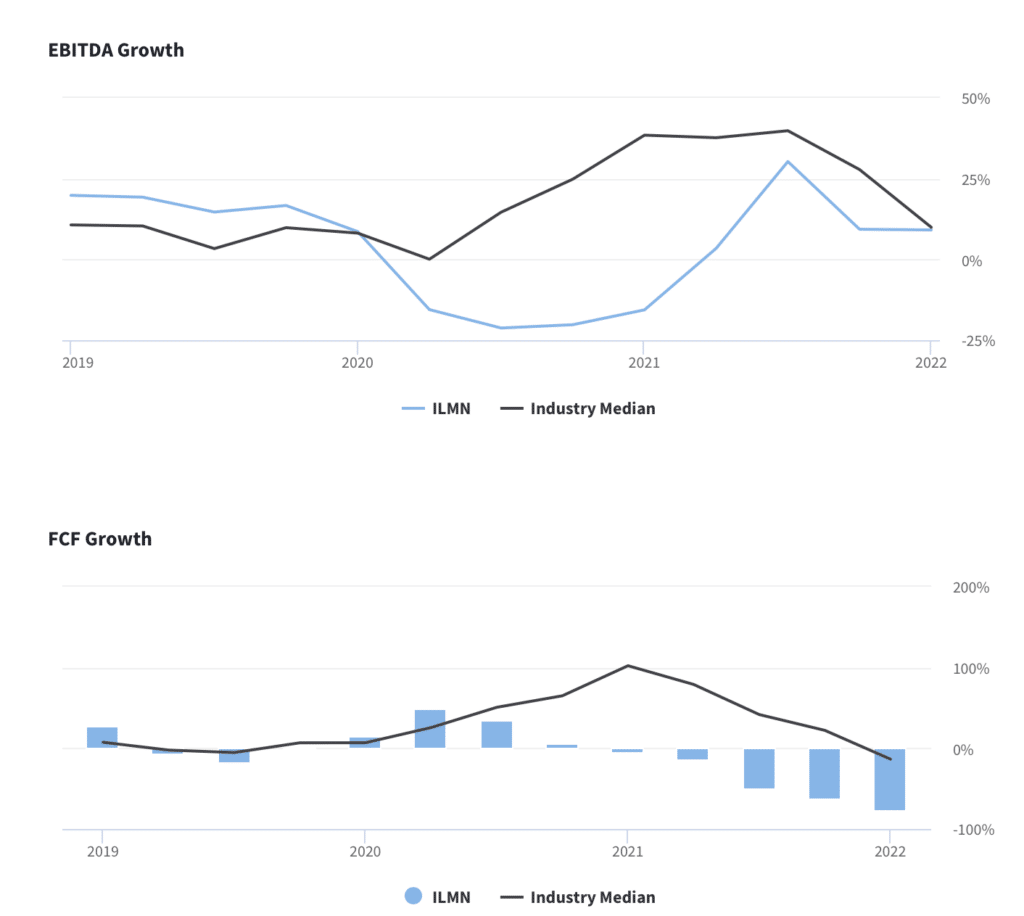

Sharper sales and profit decline relative to peers. EBITDA growth has declined since the company’s 30% peak in Q3 2021. In the most recently reported Q1, ILMN reported EBITDA growth of 9% (flat with Q4 2021 levels) and below 10% for industry peers. FCF has been negative since Q1 2021 and worsening on a sequential and YoY basis since Q2 2020. For Q1 2022 FCF was -77%, versus an industry median of -14%. Part of the more recent earnings decline can be attributed to Grail, which generated a loss of $172 million in the March quarter. Illumina has guided to Grail sales of $70M to $90M for the full year.

ILMN: EBITDA and FCF relative to peers

Regulatory risk associated with Grail acquisition. In March 2021, a bipartisan commission voted 4-0 to block Ilumina’s acquisition of Grail. citing that the acquisition would stifle competition in cancer early-detection by rivals like Guardant Health (GH) and Exact Sciences (EXAS). In August 2021, Illumina completed the acquisition– despite ongoing regulatory investigations in the EU and US. In June 2022, the FTC filed an administrative complaint and authorized a federal court lawsuit to block the acquisition. Illumina is fighting those antitrust cases and says it will appeal any adverse initial rulings. In the event of court losses, ILMN faces the risk of paying fines of $400M– in addition to divesting Grail in 2025 or 2026.

Negative surprise: CFO departs after 5 years. Earlier this month, Illumina appointed Joydeep Goswami as interim CFO while the company conducts a search for a permanent replacement. Sam Samad will be departing Illumina in July after serving as CFO for over five years and will be joining Quest Diagnostics (DGX) as its new CFO on July 11. Between Ilumina’s recent acquisition and competitive risks, Sahad’s departure comes at a crucial time for the company and heightens investor concerns about the June quarter.

ILMN: Market Snapshot

Red flag: Executive compensation. Directors were paid $0.4M, on average in 2020– well above peers and above TSR metrics.

New avenues for growth. ILMN is expanding into long-read sequencing with its new Infinity technology, while being compatible with its existing install base of 20K instruments globally. The company is working with drug developers to expand the use of sequencing inn new drug discovery. Illumina also announced a partnership with healthcare-focused investment firm Deerfield Management to use its DNA sequencing equipment in Deerfield’s start-up ventures. The goal is to encourage more biotechs to use sequencing systems and consumables.

Valuation looks rich. Valuation looks stretched, particularly given several near-term risks. As of this writing ILMN shares (~$196/share) trade at ~37x F2023E EPS and 30x F2024E EPS.

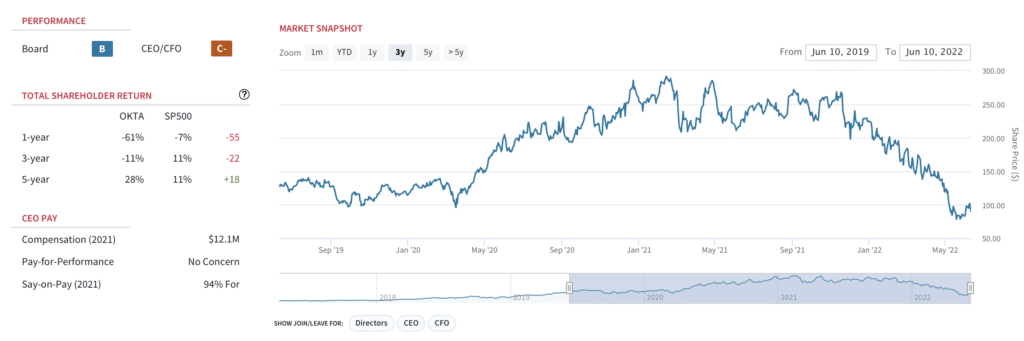

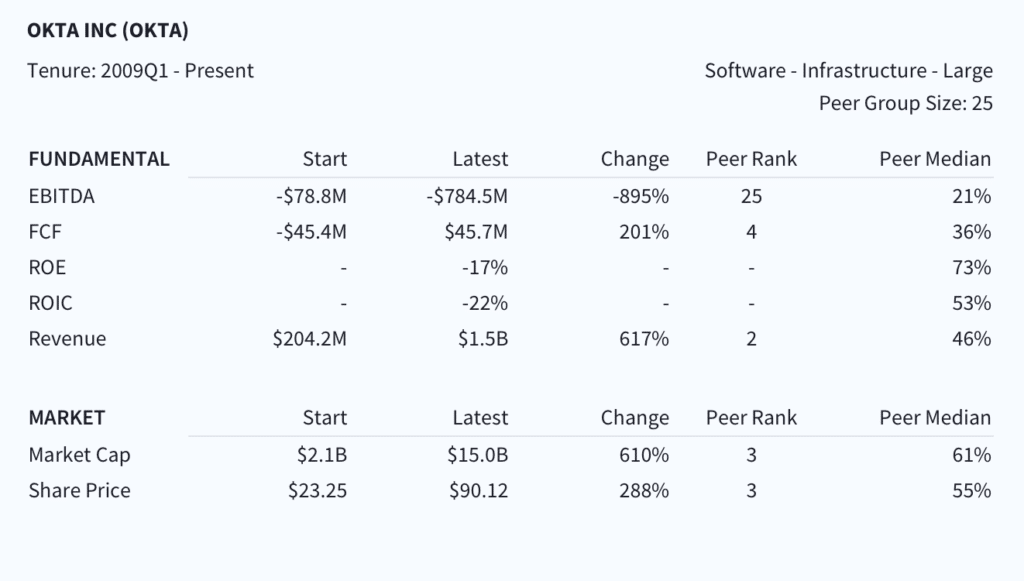

Okta (OKTA): Todd McKinnon

- Sector: Software & Infrastructure

- CEO: Todd McKinnon (13.4 years)

- CFO: Brett Tighe (1.0 years)

Cybersecurity focus with strong top line growth. With a market capitalization of $13B, Okta provides cloud-based software that helps companies manage and secure user authentication into applications as well as for developers to build identity controls into applications, web services and devices. The company is growing at >30% YoY, driven by increasing demand for cloud-based identity solutions. For F2023, Okta is guiding to 37% to 38% YoY revenue growth.

OKTA: Market Snapshot

Shares have underperformed on a 1-year and 3-year basis. OKTA shares have declined 61% over the past 12 months, versus a 7% decline for the S&P 500 over the same period. Since March of this year, after news of a security breach, OKTA shares have declined ~54%. On a 3-year basis, OKTA shares have similarly underperformed (-11% versus +11%).

Concerns that recent security breach could impact forward subscription growth. In March, Okta made headlines for a security breach that occurred in January via a third-party customer support provider. Ransomware group Lapsus$– a hacking group that claims to be behind several cyberattacks affecting Nvidia (NVDA), Samsung, Microsoft (MSFT) and others– claimed responsibility for the incident. The hacking group posted screen shots on social media of what was claimed to be Okta’s internal systems. Okta has indicated that there was no significant impact of the breach and added 800 new customers in the quarter ended April versus 650 last year. However, the company’s handling of the incident could negatively impact the momentum of its previous growth trajectory once customers begin to renew service subscriptions.

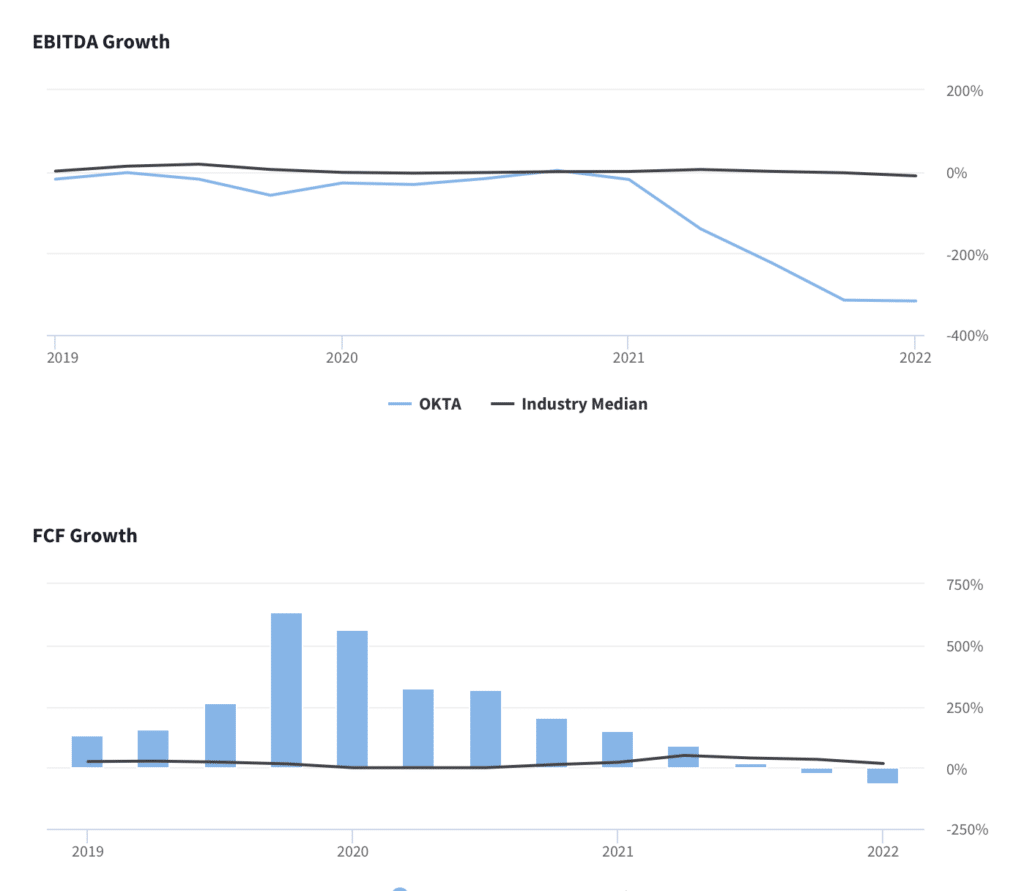

History of operating losses. Okta is spending aggressively on sales and marketing for future growth, which has resulted in large operating losses. Non-GAAP operating margin was (9.9%) in the most recently-reported quarter, the lowest levels in the past two years. Consensus estimates forecast nonGAAP profitability in F2025.

VFC: EBITDA and FCF trends

FCF and EBITDA growth are trending below peers. Since Q1 2021, EBITDA growth has declined sharply and remains well below the peer median. EBITDA growth was -317% YoY in the company’s most recently reported quarter– versus a peer median of -10%. FCF has similarly underperformed as operating expenses continue to increase. FCF declined 66% YoY in the most recently-reported quarter, versus an industry median of +16% and an increase of 153% YoY for OKTA in the year-ago quarter.

OKTA CEO Todd McKinnon: Performance Scorecard

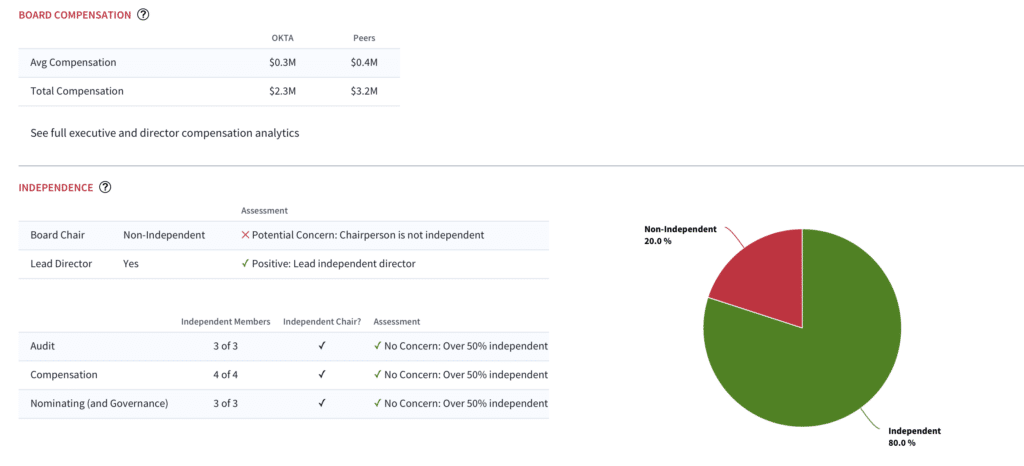

Red flag: Governance. Director Jeffrey Epstein is overboarded, serving on the boards of Couchbase, Avepoint, Poshmark and Twilio, in addition to serving as the CEO of APEX Technology Acquisition Corp. In addition, Board Chair Todd McKinnon (also CEO) is not independent.

OKTA: Governance Snapshot

Rich valuation; awaiting more evidence of earnings power. As of this writing, OKTA shares (~$83) trade at 7.8x forward sales. While we appreciate the 30% growth rate, we view the valuation as overstretched given the potential for slowing growth, high OPEX and still murky path to profitability.